I am sometimes called by journalists or other organizations who want me to confirm their biases that some company is not paying enough in tax. The conversation never goes as the journalist wishes, starts to get real complicated, as I explain that the effective tax rate the journalist is looking at takes a lot of background to understand, and that a low rate is very often nothing nefarious. This is a pretty universal sentiment among accounting professors.

Someone recently sent me a document written by Seymour Fiekowsky and issued by the Office of Tax Analysis at the U.S. Treasury Department that does an amazing job explaining this. Following is a long excerpt. But, before that long excerpt, it is fascinating to me what year this came out. 1977! 44 years ago! Amazing.

The excerpt:

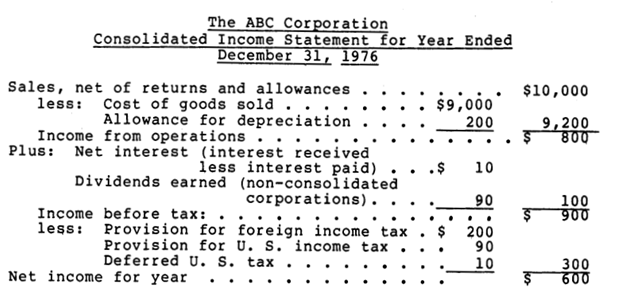

“Published income statements of corporations, including those filed with the Securities and Exchange Commission, invariably include an item labelled “Federal Income Tax.” This encourages the unwary reader to compute the ratio of this number to the preceding number, “Income Before Taxes,” and conclude that it describes the “effective” rate of tax paid by the corporation in question. In almost every case, however, the ratio thus computed tells little or nothing about the taxability of the corporation’s income. The reasons for this statement follow, but to help the reader through the discussion, the following income statement format is presented first:The automatic reflex of journalists and others unskilled in the interpretation of financial statements is to pick out the $90 for U. S. tax, divide by $900 of income before tax, and proclaim in headlines that, “The ABC Corporation in 1976 paid an effective tax rate of 10 percent, and this is less than the rate paid by their assembly line workers!” Headlines like this cause irate citizens to write to the Treasury wanting to know how the ABC Corporation has managed to avoid paying its fair share of income taxes which is supposed to be 48 percent, not 10 percent.In response, the Treasury tells them that in interpreting “effective tax rates” it is important: (1) to account for both domestic and foreign tax and income items. In the foregoing statement, $200 is reported as provision for foreign income taxes. This suggests that some part of the $900 of before-tax income has been earned abroad. Since by long-standing international conventions the United States (and other developed countries) do not “double-tax” incomes of their residents which are earned abroad and taxed there, if foreign income is to be included in the denominator of the “effective tax rate” calculation, foreign taxes should be included in the numerator.”

The rest of the document is worth reading, and it highlights issues other than the foreign/domestic income problem.

I really appreciated that someone at the Treasury spelled this all out extremely clearly (at least, based on the tax law back then), unlike some Treasury folks, who frankly seem to misunderstand the issue, and, add fuel to the fire of misinterpretation of effective tax rates and other corporate behavior.