We examine how exposure to international tax competition affects domestic firms’ employment. Consistent with prior work, we find evidence that reductions in foreign tax rates affect the domestic competitive environment via increases in import competition and investment in foreign-owned subsidiaries.

Read More

We describe the taxation landscape in the cryptocurrency markets, especially concerning U.S. taxpayers, and examine how recent increases in tax scrutiny have led to changes in crypto investors’ trading behavior.

Read More

We examine how tax-induced organizational complexity (“TIOC”), which we define as the organizational complexity that would not exist in a zero-tax world, is associated with executive performance measurement.

Read More

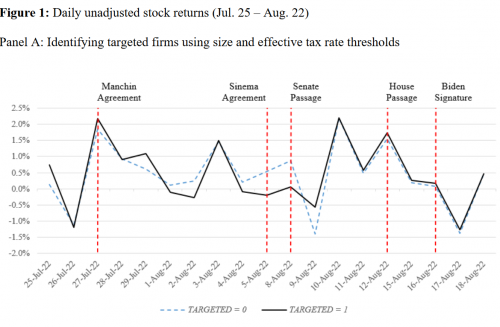

The Inflation Reduction Act establishes a new 15 percent corporate minimum tax on large U.S. corporations’ adjusted financial accounting income. While the minimum tax is estimated to raise $222 billion over 10 years, critics fear firms will manipulate their accounting earnings to reduce their tax liabilities, resulting in less revenue raised. Further, given the current political environment future legislatures could gut the tax, further eroding estimated tax revenues. Using an event study, we examine the extent to which investors believe this tax will reduce firm value. We examine stock market reactions around key legislative developments leading to the enactment of the book minimum tax. Our findings show targeted firms experience significantly lower stock returns than non-targeted firms during the enactment process (about 1.4 to 1.8 percent). In aggregate, our findings are consistent with the Joint Committee on Taxation’s revenue estimates. In cross-sectional tests, we do not observe that the firms most likely to avoid the tax via earnings management experience more positive returns, suggesting the market does not anticipate firms avoiding the tax via earnings management. Overall, our results suggest investors do not expect firms to largely avoid this tax. Instead, they expect a significant portion of the corporate minimum tax will be remitted by firms and borne by shareholders.

Read More

This paper examines the extent to which the labor market facilitates the diffusion of tax planning knowledge across firms. Using a novel dataset of tax department employee movements between S&P 1500 firms, the researchers find that firms experience an increase in their tax planning after hiring a tax employee from a tax aggressive firm. This finding is robust to various research designs and specifications.

Read More

We utilize extensive Internal Revenue Service data to investigate the tax behavior of comparable privately-held and publicly-held corporations. Our findings paint a nuanced picture of private versus public firm tax planning.

Read More

Following two decades of discussion, the border adjustment tax briefly emerged as part of proposed U.S. corporate tax reform in early 2017.

Read More

This paper examines corporations’ actions, and statements about actions, following the tax law change known as the Tax Cuts and Jobs Act (TCJA). Specifically, we examine four different outcomes — bonuses (or other actions that benefit workers), announcements of new investments, share repurchases, and dividend announcements.

Read More

We use data multinational firms provide to the Internal Revenue Service regarding their foreign subsidiary locations to explore whether some firms fail to publicly disclose subsidiaries in some countries, even when the subsidiaries are significant and should be disclosed per Security and Exchange Commission rules.

Read More

We undertake the first large-sample examination of foreign tax holiday participation among U.S. corporations. Tax holidays are temporary reductions of tax granted by governments, usually in conjunction with new business investment.

Read More

We examine whether firms hold more cash in the face of tax uncertainty.

Read More

This study provides evidence on whether investors value tax gross-up provisions for executives, and how the elimination of these provisions changes executive compensation.

Read More

We investigate the effect of public disclosure of information from corporate tax returns filed in Australia on consumers, investors, and the corporations themselves that were subject to disclosure.

Read More

We provide the first large-sample evidence of banks playing an important role in facilitating tax planning of their client firms.

Read More

This paper investigates the extent to which the expiration of a temporary tax law reduces market participants’ ability to understand corporate performance.

Read More

We investigate the relation between tax avoidance and tax uncertainty, where tax uncertainty is the possibility of losing a claimed tax benefit upon challenge by a tax authority.

Read More

We empirically investigate the effects of political uncertainty on corporate tax behavior.

Read More

We examine individual stock sales from 2008 to 2009 using population tax return data.

Read More